- Total Till grocery sales at UK supermarkets fell -1.8% YoY over the last four weeks ending 23rd April, but figures are an improvement on the -4.1% seen in March as the industry finally exited pandemic comparatives

- UK shoppers spent £10.1bn on groceries in the last four weeks, down from £10.5bn in the same period in 2021, highlighting that spending habits are returning to pre-pandemic levels

Total Till sales at UK supermarkets fell -1.8% over the last four weeks ending 23rd April, with spending during the Easter period helping to lift sales up from the -4.1% seen in March, reveals new data released today by NielsenIQ.

According to data from NielsenIQ, UK shoppers spent £10.1bn on groceries in the last four weeks ending 23rd April. This is down from £10.5bn in the same four week Easter period in 2021, but it is above the £9.6bn1 in sales recorded during the same period in 2019, highlighting a rebalancing of supermarket spend as UK shopping behaviour returns to pre-pandemic levels.

Data from NielsenIQ shows that in the last four week period there was a slight decline in the number of items in the basket (11.2 items compared to 11.5 in March).2 This data suggests that shoppers are now more cautious of how much they are spending and are prepared to make trade-offs around the number of items purchased.

Shoppers start to resume a more normal lifestyle

Whilst online sales fell 18.5% compared to a year ago, shopper penetration is holding at 26.5% of households. This further highlights the rebalancing of basket spend; as shopping behaviours normalise, this is reflected in smaller online basket spend. Meanwhile, in-store sales are growing (+0.8%) and visits to stores are up 5.1%. This has impacted the online share of grocery spend, which has now fallen to 11.8%, the lowest since April 2020 (with the exception of Christmas 2021 when it was 11.2%).

In terms of what shoppers are spending their money on, the strongest super category in the last four week period was confectionery (+35%) which was aided by the timing of Easter. This was closely followed by pet and petcare (+13.6%), health and beauty (+8.3%), soft drinks (+3.3%) and delicatessen (+2%). Within these categories, mineral waters (+11%), deodorants/sprays (+16%), sandwiches (+21%) and suncare (+29%) all reflect the return to pre-pandemic lifestyles as shoppers travel more, engage in more activities on the go and plan ahead for holidays. Following concerns over cooking oil shortages, NielsenIQ data also shows that the value sales of oils increased by 29%.3

However, data from NielsenIQ reveals that there was a decline in sales for beers, wines and spirits (-15.9%), meat, fish and poultry (-7.8%) as well as frozen food (-7.5%). In particular, volume sales fell 13% in meat, fish and poultry, which could indicate that shoppers are moderating their purchasing in this category. 3 This is confirmed in a recent NielsenIQ survey where 28% said this is the number 1 category where they would save money on their grocery spend.4

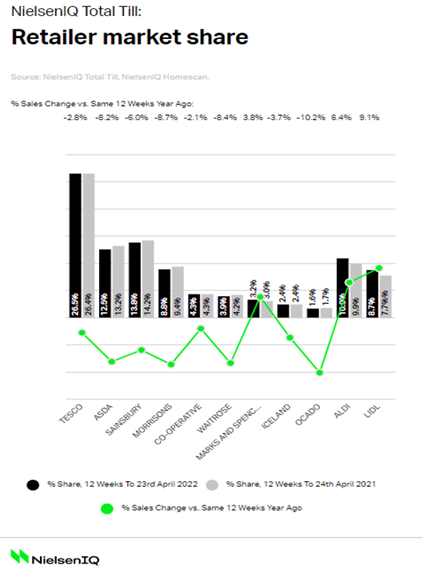

In terms of retailer performance, Aldi (+6.4%) and Lidl (+9.1%) led the market in terms of growth. Tesco was the only retailer of the ‘big 4’ supermarkets to have gained market share and M&S’ performance remains strong.

Mike Watkins, NielsenIQ’s UK Head of Retailer and Business Insight, said: “Easter is a catalyst for sales growth and if a later Easter lands with warm weather, this can really help drive footfall. This was the case last year, which also coincided with the end of the final lockdown, giving a one-off boost to supermarket sales. Although sales this year are subdued, they are still above levels recorded pre-pandemic in 2019, and indicates the start of normal shopping behaviours returning, which now includes a wider choice of where to shop: online, in store or a mix of the two.”

Watkins continues: “However, it is clear that as cost-of-living increases continue, retailers will be looking to make sure they offer the best value for money. Promotional spend has already moved up to 21.5% of value sales, and whilst in this instance this reflects seasonal promotions, this could also herald the start of more pricing activity in the weeks ahead, such as private label price cuts and more targeted promotions through loyalty schemes. With this in mind, it will be important for retailers and brands to adapt ranges and prices to help maintain sales momentum in Q2 and into the start of summer.”

Table: 12-weekly % share of grocery market spend by retailer and value sales % change

Unless otherwise stated all data is NielsenIQ Homescan Total Till

1 Four weeks ending 27/4/2019. NielsenIQ Scantrack Grocery Multiples

2 Homescan FMCG GB

3 NielsenIQ Scantrack Grocery Multiples

4 NielsenIQ Homescan Survey

Comments are closed.