- With gloomy weather towards the end of July and early August, Total Till slowed to +7.2% – the lowest since January. Sales peaked in June at +12.4%.

- Retailer promotional activity increased to 23%, up from to 22.5% recorded in the previous month in a bid to encourage shoppers to spend more.

- In-store sales (+7.9%) maintain stronger growth ahead of online sales (+3.8%) over the last four weeks.

Total Till sales at UK supermarkets slowed to +7.2% in the last four weeks ending 12th August 2023 according to new data released today by NIQ (previously known as NielsenIQ).

According to NIQ, this drop in sales is due to lower inflation as well as unsettled, unseasonable weather over the summer months, with shoppers visiting stores fewer times (-0.5%) in the last 4 weeks compared to the same period last year. With the upcoming bank holiday weekend, shoppers caution is expressed in weaking volume sales at the Grocery Multiples weakening to -3.8% compared to -3.6% in July.

Retailers have further increased spend on promotional activity (23%) compared to the previous month (22.5%) on all FMCG goods in a bid to ease the effects of the cost-of-living crisis and encourage spending. There have been targeted price cuts by most retailers and loyalty cards used to assist with savings as inflation starts to slow.

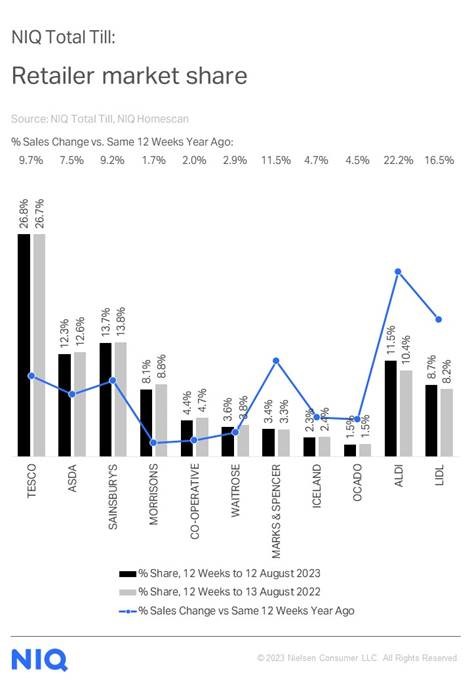

NIQ data also highlights that Tesco saw an increase in sales (+9.7%) and gained market share over the latest 12 weeks attracting both new shoppers and an increase in in-store visits; Aldi (+22.2%), Lidl (+16.5%) and M&S ( +11.5%) were the only other retailers who gained market share in this period.

The trend for bargain hunting continues with 62% of consumers shopping at Discounters in the last four weeks and over 780,000 new shoppers at Discounters compared to this time last year1. The retailers with the weakest growth were Morrisons (+1.7%) and Co-Op (+2.0%) ,with the Co-Op more impacted by comparisons against the summer 2022 heatwave.

Mike Watkins, NIQ’s UK Head of Retailer and Business Insight, said: “Recent weeks have seen a decline in supermarket volumes, likely influenced by factors such as summer holidays and unpredictable weather. The rising cost of living also continues to deter people from dining out, with 53% of consumers attributing this decision to increased prices for eating and drinking out 2. The inclement weather has similarly affected non-food retail, as indicated by the recent BRC KPMG retail sales monitor. It’s evident that encouraging consumer spending has become an industry challenge, extending beyond just grocery shopping.

“Despite lower inflation, most consumers remain pessimistic about their financial situation in the coming three months, with 60% anticipating that they will be severely or moderately impacted by rising living costs3. With the added concerns of increasing mortgage and rental expenses for many households, it appears that a shift in sentiment may be some time off and as a result, while Total Till growth will continue to decelerate as inflation eases, it will still be difficult for retailers and manufacturers to drive fmcg volume growths”.

Table: 12-weekly % share of grocery market spend by retailer and value sales % change

Unless otherwise stated all data is NIQ Homescan Total Till

Unless otherwise stated all data is NIQ Homescan Total Till

1 NIQ Homescan FMCG 4 week to 12th August 2023

2 CGA Cost of Living Consumer Pulse, July 2023.

3 NIQ Homescan Survey July 2023

Comments are closed.