- Total Till sales stabilise at UK supermarkets, falling -3.4% over the last four weeks ending 26th February, similar to the -2.9% seen in January

- UK supermarkets experience a 4.4% uplift in sales compared with pre-covid levels two years ago, indicating a new baseline for sales growth

- However, inflation at UK supermarkets continues to grow and as we exit COVID-19, new challenges lie ahead amid the threat of disruption to global food supply and soaring energy and fuel costs that will impact shopper budgets

Grocery sales at UK supermarkets stabilised in February, with total till sales falling -3.4% over the last four weeks ending 26th February. This is similar to figures reported the previous month, where sales fell -2.9% in January, reveals new data released today by NielsenIQ.

Brits spent £9.7bn at the grocery multiples1 over the last four weeks, down -4.2% compared with last year. But there is a 4.4% uplift in sales compared with pre-covid levels two years ago, which indicates there is now a new baseline for sales growth. Moreover, as shopping behaviour normalises, industry spend per visit is stabilising at £18.502, compared to £21.10 this time last year and is now close to the £17.20 of February 2020, further suggesting the end of COVID-19 trendlines.

Further to this, data from NielsenIQ reveals that the online share of all FMCG sales fell back to 12.5% in the last four week period (from 13.1% in January), with sales down 20% compared with the same period last year. In contrast, visits to stores are up 12% which is helping to support ‘brick and mortar’ growth (+0%), and sales in convenience channels also continue to improve (+3.3%)3.

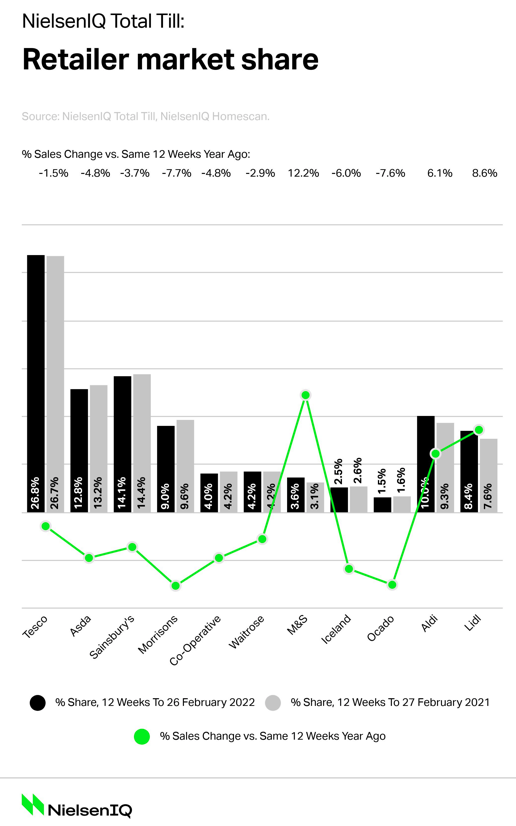

In terms of retailer performance, Marks & Spencer was the fastest growing retailer over the last 12 weeks (+12.2%) as shoppers returned to retail parks, the high street and travel outlets and market share increased to 3.6%, the highest since Q4 2017. Discounters Lidl (+8.6%) and Aldi (+6.1%) also experienced growth and attracted new shoppers due to new store openings. According to NielsenIQ, 1 in 3 of all households shopped at Lidl and almost 40% at Aldi in the last four weeks ending 26th February 2

However, retailers are warned that shopper habits are set to change once again as inflation grows and supermarkets are impacted by global food supply disruption. What’s more, soaring energy and fuel costs will impact shopper budgets more generally. In a new study from NielsenIQ which explores how consumer behaviour differs across the economic spectrum 4, 19% of UK shoppers are classed as ‘strugglers’, having experienced job or income loss due to COVID-19 which is still affecting them today – this is compared to 23% at a global level.

Mike Watkins, NielsenIQ’s UK Head of Retailer and Business Insight, said: “Although we are seeing a stabilisation of shopper spend, inflation at supermarkets has increased since the start of the year to +2.7%5, the highest we’ve seen since September 2013. The pandemic may soon be behind us, but new threats are on the horizon. Global food supply disruption and soaring energy and fuel costs, are set to impact shopper baskets and have the potential to slow down any growth in supermarket volumes.

Watkins adds: “With promotional spend unchanged at 20%2 of sales purchased, we can instead see a sharpening of pricing activity with price matches, price cuts, couponing, fuel vouchers, and comparative shopping basket advertising. Many supermarkets with a loyalty scheme have also offered differential price discounts as well as personalised offers which have the potential to drive frequency of visit as well as mitigate some of the impact of rising food prices. Retailers and their suppliers must be prepared for the uncertainty that lies ahead and ensure they are taking every step possible to support shoppers in balancing budgets over the next few months.”

Table: 12-weekly % share of grocery market spend by retailer and value sales % change

1NielsenIQ Scantrack ‘Grocery Multiples’ : a defined subset of the major supermarkets that also includes all food sales from Marks and Spencer (but excludes Aldi and Lidl)

2 NielsenIQ Homescan FMCG

3 NielsenIQ Scantrack Convenience

4 `A new economic divide will fragment the retail landscape of 2022`. NielsenIQ, February 2022

5 BRC-NielsenIQ Shop Price Index (SPI)

Comments are closed.