- Total Till sales for the four weeks ending 9th September 2023 improved +10.3%, up from +7.2% during the wet July and early August

- Sunny weather encouraged more shoppers to visit stores (+4.9%) with sales in store experiencing a 10.6% uplift in the last four weeks, compared to online growth (+7.3%)

- Sales of meat, fish & poultry (+10.4%) and produce (+11.8%) proved popular with shoppers as temperatures soared

The late summer and unexpected heatwave in early September helped lift grocery sales at UK supermarkets, with Total Till sales growing +10.3% in the last four weeks ending 9th September 2023, compared with the same period last year, reveals new data, released today by NIQ (previously known as NielsenIQ).

Data from NIQ reveals that growth at the grocery multiples (supermarkets) during the four week period increased by +7.2%, and peaked at 10.2% in the week ending 9th September, in which the UK experienced a heatwave. Volume sales during this week also improved to +2.1% for the first time since the first week of May 2023 suggesting improved consumer willingness to spend. Volume sales over the four week period stabilised at -0.7%, but this is up from -3.8% last month.

Despite online sales growing behind bricks and mortar a quarter of GB households continue to shop online in the last four weeks confirming shoppers are still embracing an omnichannel experience. 1

Brits spend more on seasonal foods

As temperatures soared, this encouraged Brits to visit stores and loosen their purse strings and purchase more fresh food items. A total of £172m was spent on fresh poultry (value sales +13% and volumes +5%) in the four week period, with chicken thighs and drumsticks (+28% value sales, volumes +15%) proving popular.

Sales also grew for fresh produce (value growth of +11.8% with volumes +2.1%) which included seasonal foods such as tomatoes (volumes +1.5%) and lettuce (volumes 3.9%). The end of summer clearances and back to school promotions also led to an uplift in volume sales for general merchandise items (+1.7%) as shoppers were offered one-off bargains at most of the big supermarkets. 2

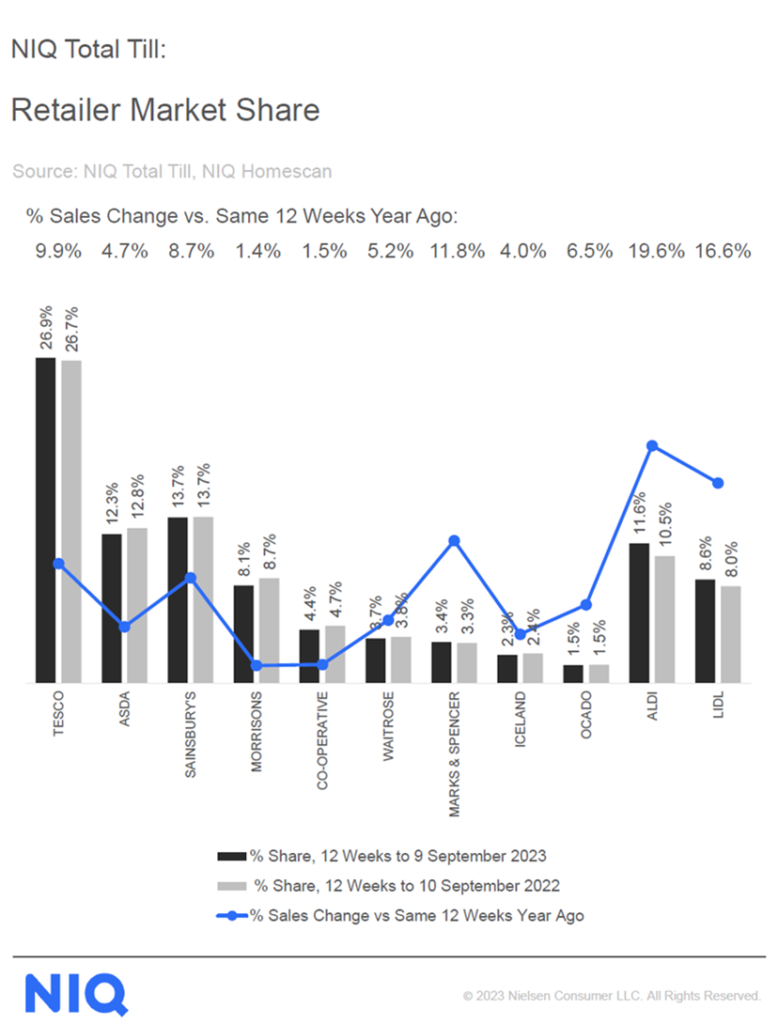

Tesco, M&S and discounters grew market share over the 12 weeks

Over the full 12 week period Total Till growths were 8.9%. In terms of retailer performance nearly 1 in 3 households shopped at M&S – almost the same as Co-op – with sales growth (11.8%) helped by the opening of new Foodhalls across the country. Tesco (+9.9%) also gained market share with Sainsbury’s share holding firm (+8.7%) with both retailers using price cuts delivered through Clubcard and Nectar loyalty schemes to drive top line growth as inflation started to slow.

This is in tune with current shopper needs, with data from NIQ’s recent Consumer Outlook Mid-year report showing that the most important saving strategies at the moment are shopping at stores with loyalty points and using loyalty points to manage spend, and opting for private label.

However, it is Aldi (+19.6%) and Lidl (+16.6%) who are outperforming across all shopper metrics with new shoppers, more visits and higher spend per visit contributing to a market share of 20%.

Mike Watkins, NIQ’s UK Head of Retailer and Business Insight, said: “The warm weather has led consumers to shop more in-store, but online penetration remains unchanged in the last four weeks which has been an underlying trend this year. Shoppers are still using this channel but habits have changed. As they visit stores more often, consumers are reducing grocery spending online as they shop around to find the best prices. Shoppers go into a store around four times a week but place online grocery orders on average around twice a month.”

Watkins continues: “There are some improvements showing in shopper sentiment as inflation continues to slow and there is now a growth in real incomes. Retailers are keen to pass on price cuts as inflation continues to slow. However, they also need to make sure that messages resonate with price conscious consumers, as for some, their discretionary spending power is still limited. We know there is a polarisation of purchasing power with 44% of households impacted only a little or not at all by increased cost of living yet 56% of households are moderately or severely affected, leaving them budgeting carefully.3 The good news is that FMCG volumes are starting to improve against the declines of last year so we expect Total Till growth to be around 7% in Q4 and volume growth at food retailers in December.”

Table: 12-weekly % share of grocery market spend by retailer and value sales % change

Unless otherwise stated all data is NIQ Homescan Total Till

Unless otherwise stated all data is NIQ Homescan Total Till

1NIQ Homescan FMCG

2NIQ Scantrack Grocery Multiples

3NIQ Homescan Survey July 2023

Comments are closed.