- Total Till sales at major supermarkets grew (+3.3%) while unit growth (-0.8%) continues to decline.

- 35% of all growth in FMCG sales since the start of the year has come from ecommerce, with the rapid delivery channel capturing a 22% share of online chocolate confectionery sales over the Valentine’s Day weekend.

-

Shoppers focus on purchasing fresh categories with dairy (+2.2%), produce (+1.3%) and meat/fish/poultry (+0.4%) the only supercategories experiencing unit growth.

Total Till sales at UK major supermarkets grew (+3.3%) in the last four weeks ending 21st February 2026, according to new data released today by NielsenIQ (NIQ). Despite this growth, NIQ data shows the unit growth declined from January (-0.8% from -0.6%), indicative of continued pressure on shopper wallets.

Inflation has continued to ease (+3.5% from 3.9%)1; however, shoppers are purchasing less and altering their buying habits as consumer demand across all channels remains unpredictable. In addition, the impact of a decline in Consumer Confidence (GfK Index of -19 in February from -16 in January) was felt by food retailers who relied on shoppers spending more around the key calendar events during this period, including half term, Valentine’s Day, Pancake Day and the run up to Chinese New Year.

As well as shoppers spending £42m on rice, grains and noodles, shoppers also purchased more accompaniments to make up a celebratory Chinese New Year meal occasion spending £6.8m on oriental cooking sauces (+10.9%) and £3.4m on fresh savoury snacks (+32%).2

As part of the seasonal dine-in deal offers, shoppers spent £58.5m on own label fresh ready meals (+3.4%)2 of which 45% were premium own label; an attractive alternative to eating out. Also, during the week of Valentine’s Day, shoppers harnessed the convenience and immediacy of treating loved ones by using rapid delivery, with this channel having a 22%3 share of online chocolate confectionery sales for the Valentine’s Day weekend.

For the first time in over a year, NIQ data shows that there was a dip in the frequency of shopping, perhaps not helped by the wet weather, but a growth in the number of items in the basket helped by eCommerce. In fact, 35% of all growth in FMCG sales since the start of the year has come from eCommerce.4 As such, eCommerce (+9.2%) remains the fastest-growing channel in terms of value sales growth and continues to increase its market share, increasing to 14.2%.

The reluctance to spend is illustrated with only three super-categories in unit growth; dairy (+2.2%), produce (+1.3%) and meat/fish/poultry (+0.4%).5 This is supported by data that shows 33%6 of shoppers are changing the way they shop to save money, rising to 58% for those who feel severely impacted by the cost of living.

Further more, the gap between own label unit growth (+1%) and branded unit growth (-2.2%) continues to widen, with 15% of household shoppers saying they are saving money by switching to own label products, 16% choosing cheaper brands and 18% shopping more at Discounter stores.

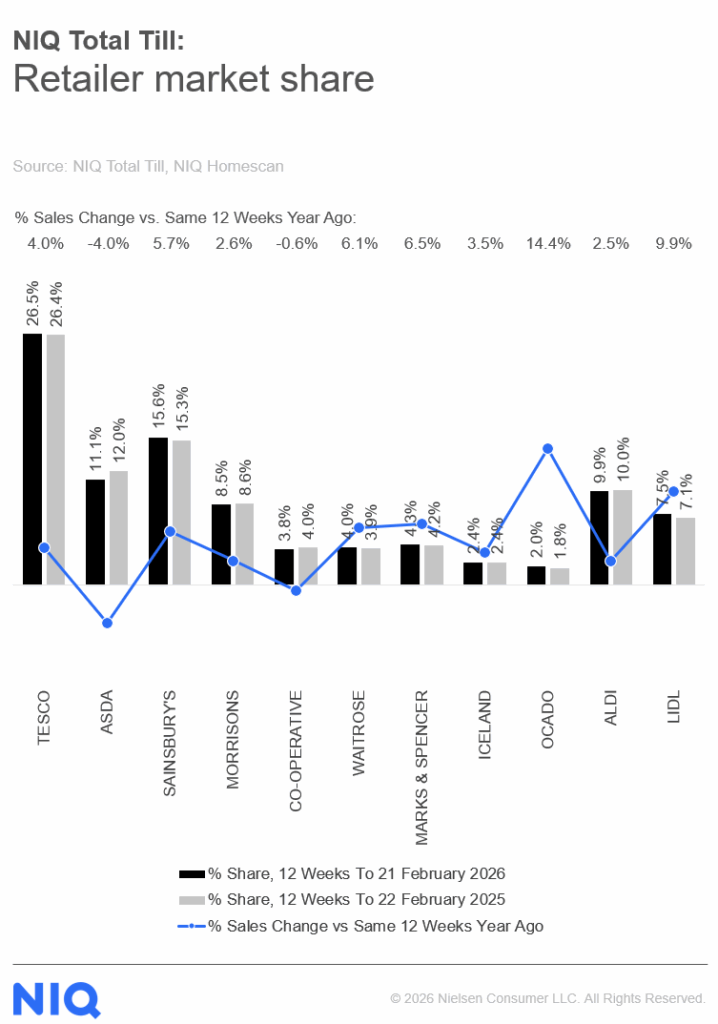

Ocado (+14.4%) continues to gain market share, retaining its position as the fastest-growing retailer, followed by Lidl (+9.9%). Helped by their respective offers for Valentine’s day, both M&S (+6.5%) and Waitrose (+6.1%) also gained market share and the frequency of store visits was higher than last year.

Mike Watkins, Head of Retailer and Business Insight at NielsenIQ, said: “Many retailers focused on attracting shoppers with a choice of dine-in deals to capture a bigger share of spend at out-of-home channels, with premium offers such as three courses for two people for £25 setting a new and attractive price point compared to eating out.

He adds: “In fact, there was a small increase in basket size in the last four weeks and whilst it is too soon to say if this is a turning point in shopper behaviour, these big events encouraged shoppers to spend more and it’s possible that some are bringing some spend forward to help manage budgets ahead of Easter.”

Unless otherwise stated all data is NIQ Homescan Total Till.

Unless otherwise stated all data is NIQ Homescan Total Till.

1 BRC NIQ SPM February

2 NIQ Scantrack, Total Coverage, 1w.e 14th February 2026

3 NIQ Digital Purchases 13th/14th/15th February 2026

4 NIQ Scantrack E-commerce (Defined Grocery Multiples)

5 NIQ Scantrack, Total Coverage, 4 we 21.02.26

5 NIQ Homescan Survey November 2025

Comments are closed.