- Take-home sales at the grocers rose 3.4% in the four weeks to 22 February 2026 compared with a year ago.

- Online grocery records highest channel share since July 2021.

- Spending on premium dine-in meal deals in the week of Valentine’s Day hits £39 million.

![]() Take-home sales at the grocers increased by 3.4% in the four weeks to 22 February 2026 compared with the same period last year. Like-for-like grocery price inflation rose slightly to 4.3%, having fallen in each of the previous four months.

Take-home sales at the grocers increased by 3.4% in the four weeks to 22 February 2026 compared with the same period last year. Like-for-like grocery price inflation rose slightly to 4.3%, having fallen in each of the previous four months.

Shoppers increasingly chose to get their shopping done online, with sales made through the internet up 9.7% year on year. More than 18 million orders were placed over the four weeks, taking the channel’s share to 13.0%, the highest level since July 2021.

Fraser McKevitt, Head of Retail and Consumer Insight at Worldpanel by Numerator, said: “More affluent families in London and the Southeast of England are still the most likely to shop for groceries online. However, the channel’s appeal is broadening, with shoppers from a wider range of economic backgrounds increasingly drawn to its convenience.”

Valentine’s Day shoppers leave love to the last minute

Shoppers dialled up the romance at home this Valentine’s Day, splashing out on premium dine-in experiences. Spending on high-end meal deals, priced at £10 or more, hit £39 million in the week of Valentine’s Day, seven times higher than the previous week.

The uplift in meal deal spending began in the middle of the week, with sales accelerating from Wednesday 11 February, alongside a noticeable pop in sparkling wine purchases. But many left it to the last minute, as nearly 12% of households picked up a premium meal deal on Friday night alone.

Steak buyers sprang into action later in the week, with sales peaking on Friday 13 and Saturday 14 February. Chocolate lovers also left it late, with Friday the single biggest day of purchasing of Valentine’s Day chocolate.

Pricey pancakes set the tone for Easter

Sales of pancake ingredients surged in the seven days leading up to Shrove Tuesday, with flour up 34%, sugar rising by 17% and lemons soaring by 70% as shoppers stocked up for the annual tradition.

Demand for convenience was also clear, with sales of pre-made pancake mixes more than doubling in the week (+114%). However, those flipping their own this year paid slightly more for the privilege, as the cost of key ingredients reached £7.77*, an increase of 42p or nearly 6% on last year.

McKevitt added: “Looking ahead to Easter, shoppers will notice that chocolate prices remain high, up 9.3% year on year. While this is still a significant rise, the pace of inflation in the category is beginning to ease and is now at its lowest level since September 2025.”

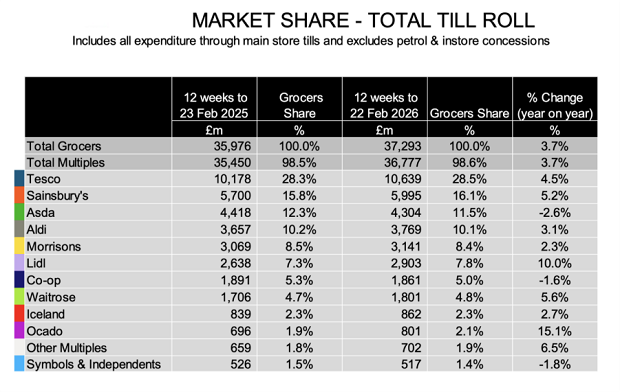

Over the 12 weeks to 22 February 2026, Ocado was once again the fastest growing grocer, a position it has maintained since September 2025. With sales up by 15.1%, the online specialist’s market share hit 2.1%, up from 1.9% in the corresponding 12 weeks in 2025.

Lidl recorded double-digit sales growth for the twelfth consecutive period, up this time by 10.0%. Taking an additional 0.5 percentage points of share, the discounter outpaced bricks and mortar competitors and now accounts for 7.8% of the market.

Sainsbury’s increased market share to 16.1%, up from 15.8% a year ago, as sales rose by 5.2% over the 12 weeks. The retailer attracted an additional 400,000 shoppers through its doors during the period.

Tesco, Britain’s largest grocer, saw sales grow by 4.5%, lifting market share to 28.5%, 0.2 percentage points higher than in 2025.

Sales at Waitrose, part of John Lewis partnership, grew 5.6% – the grocer’s highest rate of growth recorded since March 2021. Market share increased to 4.8%, up from 4.7% last year, the highest level in three years.

Sales at Aldi rose by 3.1% year on year, delivering a 10.1% share of the market. Iceland maintained a 2.3% share, with sales up 2.7%, while Morrisons holds 8.4% of the market following a 2.3% increase in sales. Asda and Co-op account for 11.5% and 5.0% of the take-home grocery market respectively.

M&S, while not a grocer, is a major competitor to the supermarkets in the chilled ready meals category which featured so heavily in shoppers’ Valentine’s Day baskets. Grocery sales at M&S were 7.0%** higher over the 12 weeks compared to last year.

* Based on the average price paid for 4 pints of milk, 1.5kg plain flour, 1kg caster sugar, 6 eggs and a bag of lemons.

**Please note: with a higher proportion of clothing and general merchandise in its sales mix, M&S does not fall under the definition of ‘grocers’ using the Till Roll methodology on which the Worldpanel Grocery Market Share release is based. For this reason, a comparable market share number is not provided for M&S. The M&S growth number quoted in this update is for FMCG sales only, while the figures for grocers in the Grocery Market Share table cover total spending through supermarkets’ tills.

An update on inflation

Grocery inflation now stands at 4.3% for the four-week period ending 22 February 2026. Prices are rising fastest in markets such as, fresh unprocessed meat, skin care and chocolate confectionery and are falling fastest in chilled butter & spreads, household paper and sugar confectionery.

This figure is based on over 75,000 identical products compared year on year in the proportions purchased by British shoppers and therefore represents the most authoritative figure currently available. It is a “pure” inflation measure in that shopping behaviour is held constant between the two comparison periods – shoppers are likely to achieve a lower personal inflation rate if they trade down or seek out more offers.

Worldpanel by Numerator’s data visualisation tool allows you to view and analyse grocery market share data online. The latest sales share figures for all of the major grocers can be viewed and compared with historical figures and all graphics within the Worldpanel dataviz are available to embed in your site.

Comments are closed.